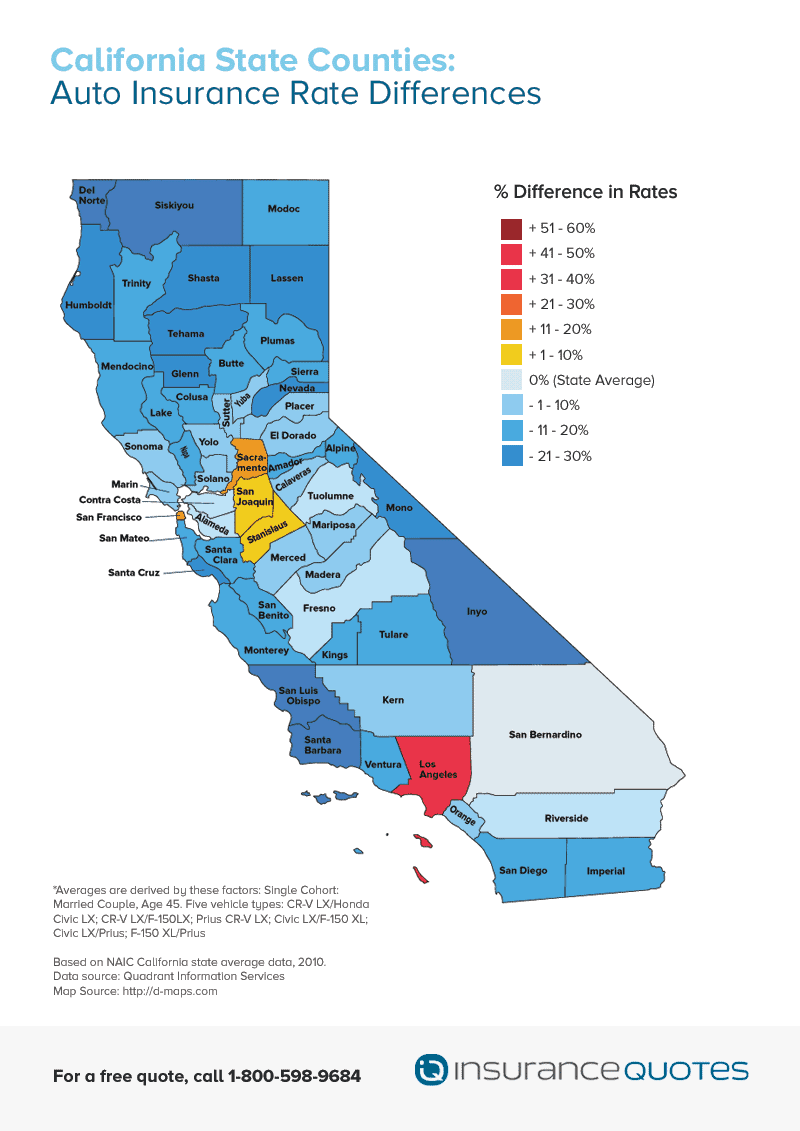

Californias Car Insurance Premiums Are Rising Too Which Bay Area Cities Pay More

California Car Insurance Premiums Are Rising: Which Bay Area Cities Pay More?

California car insurance premiums are experiencing a significant upward trend, a phenomenon impacting drivers across the state. This surge is not uniform, however, with certain geographic locations within the densely populated Bay Area bearing a disproportionately higher burden of these escalating costs. Understanding the contributing factors and identifying the specific cities most affected is crucial for residents navigating this challenging insurance landscape. Several interconnected forces are driving these increases, ranging from broader economic pressures to localized risk factors.

One of the primary drivers of rising car insurance premiums in California, and consequently the Bay Area, is the escalating cost of vehicle repairs. Modern vehicles are increasingly equipped with sophisticated technology, including advanced driver-assistance systems (ADAS) like adaptive cruise control, lane-keeping assist, and automatic emergency braking. While these features enhance safety, they also significantly increase the complexity and expense of repairs after an accident. Sensors, cameras, radar units, and specialized computer modules are often integrated into bumpers, windshields, and other structural components. Replacing or recalibrating these parts can cost thousands of dollars, directly translating into higher claims costs for insurers, which are then passed on to policyholders in the form of increased premiums. Furthermore, the proliferation of electric vehicles (EVs) and hybrid models, while environmentally beneficial, also presents unique repair challenges and associated costs that contribute to the overall premium inflation. The specialized knowledge and equipment required to service these vehicles, coupled with the cost of battery replacements, add another layer to the repair expense.

Another substantial contributor to rising California car insurance rates is the increasing frequency and severity of vehicle thefts. While theft rates can fluctuate, certain urban areas, including parts of the Bay Area, experience higher incidences of car break-ins and outright vehicle theft. Organized crime rings and opportunistic thieves alike target vehicles for their valuable components, such as catalytic converters (due to the precious metals they contain), or for the entire vehicle itself. Insurers factor in the statistical probability of a policyholder experiencing theft in a given area when setting premiums. Areas with higher reported theft rates will naturally see higher insurance costs. The economic impact of these thefts extends beyond the direct financial loss for individuals; it contributes to increased claims payouts for insurers, further driving up overall premium costs for everyone in that region. Law enforcement efforts and anti-theft technologies play a role in mitigating these risks, but the persistent challenge of vehicle theft remains a significant factor in California’s escalating insurance market.

The sheer density of vehicles and the associated traffic congestion within the Bay Area also play a pivotal role in elevated car insurance premiums. With a high concentration of drivers on a limited road network, the likelihood of accidents increases. Frequent traffic jams, aggressive driving behaviors, and the sheer volume of vehicles sharing the road contribute to a higher statistical probability of collisions. Insurers assess risk based on empirical data, and areas with a greater number of reported accidents, regardless of their severity, will invariably have higher premiums. The Bay Area’s complex network of highways and urban streets, often subject to gridlock, creates a high-risk environment for drivers. Even minor fender-benders can lead to significant delays and increased opportunities for secondary accidents, further exacerbating the problem. This constant exposure to potential collisions directly influences the actuarial calculations used by insurance companies to determine risk and, consequently, premium pricing.

The inflationary environment affecting the broader economy has also seeped into the car insurance sector. The cost of goods and services across the board has risen, and this includes the components and labor required for auto repairs. The price of replacement parts, from tires and batteries to more complex electronic modules, has increased. Similarly, labor costs for auto mechanics and body shop technicians have gone up due to rising wages and the demand for skilled professionals. These increased operational costs for repair facilities are ultimately passed on to insurers, who, in turn, adjust policy premiums to maintain profitability. The general increase in the cost of living means that even minor repair bills become more substantial, contributing to the overall upward pressure on insurance rates throughout California.

Specific Bay Area cities often exhibit higher car insurance premiums due to a combination of the aforementioned factors, with localized data often revealing significant disparities. While precise, up-to-the-minute figures can vary by insurer and policy specifics, several cities consistently appear at the higher end of the premium spectrum.

San Francisco frequently ranks among the priciest for car insurance in the Bay Area and California. Its dense urban environment, high traffic volume, and documented issues with vehicle break-ins and thefts contribute to elevated risk profiles. The narrow streets, limited parking, and the sheer concentration of vehicles make accidents more probable, and the city’s reputation for property crime, including car theft, directly impacts insurance calculations. The cost of living in San Francisco is also among the highest in the nation, which can indirectly influence repair costs and labor rates.

Oakland, with its own significant traffic congestion, higher reported crime rates including auto theft, and a large population, also tends to see higher car insurance premiums. Similar to San Francisco, the urban density and the challenges of navigating city streets contribute to a greater likelihood of accidents. The economic factors and the cost of doing business in the East Bay also play a role in the overall expense of claims.

Cities within San Mateo County, particularly those closer to the urban core like Daly City, can also experience higher rates. Their proximity to San Francisco means they often share some of the same traffic and crime-related risks. The high population density and the reliance on personal vehicles for commuting in and out of the city contribute to traffic volumes.

Parts of Alameda County, beyond Oakland, such as Hayward and Union City, can also see elevated premiums due to their own demographic profiles, traffic patterns, and localized crime statistics. These cities are often part of major commuting corridors, leading to increased congestion and a higher potential for accidents.

Fremont, while generally less dense than its northern counterparts, still experiences considerable traffic congestion due to its role as a major employment hub and its position along key transportation routes like I-880 and I-680. The sheer volume of vehicles and the potential for accidents on these busy freeways contribute to insurance costs.

It’s important for Bay Area residents to recognize that while these cities are often cited for higher premiums, individual circumstances remain paramount. Factors such as driving record, age, vehicle type, coverage levels, and the specific insurance provider all significantly influence the final premium amount. Nevertheless, geographic location within the Bay Area undeniably plays a substantial role in the escalating cost of car insurance for many Californians.

{kind=link}