Off The Charts Natural Disaster Costs

Off the Charts: Unpacking the Astonishing Economic Toll of Natural Disasters

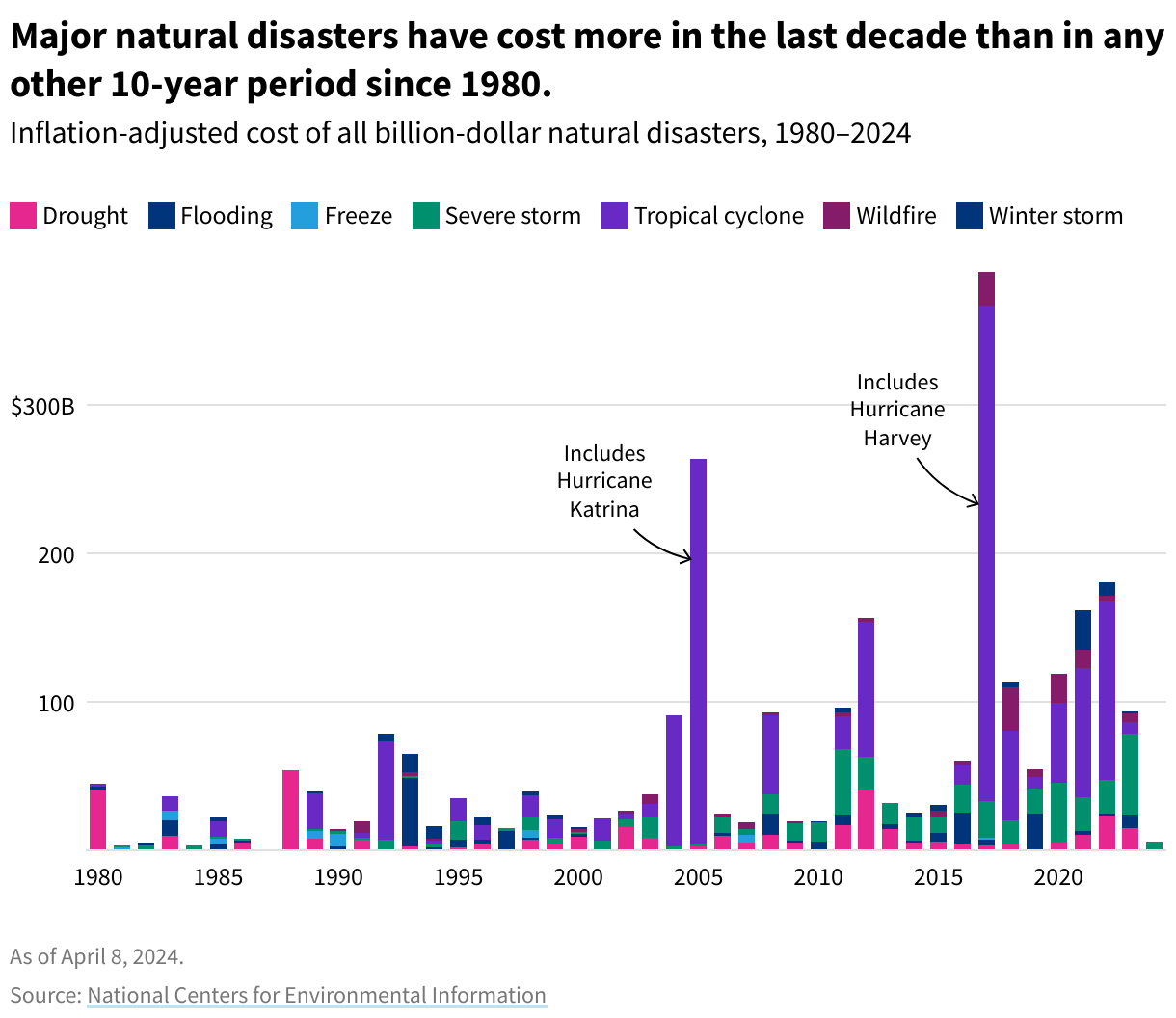

The escalating frequency and intensity of natural disasters are inflicting unprecedented economic damage globally. Beyond the immediate devastation and tragic loss of life, the financial repercussions are cascading through local economies, national budgets, and international markets. Understanding the magnitude of these costs, from direct damages to long-term recovery and adaptation expenses, is crucial for effective risk management, policy formulation, and sustainable development. This article delves into the multi-faceted economic impacts of natural disasters, highlighting trends, identifying key drivers of escalating costs, and exploring the financial implications for various stakeholders.

Direct economic losses represent the most immediate and quantifiable consequence of natural disasters. These encompass the physical destruction of infrastructure, buildings, homes, agricultural assets, and natural resources. For instance, hurricanes can obliterate coastal communities, leaving behind billions of dollars in property damage. Earthquakes can reduce entire cities to rubble, destroying critical infrastructure like roads, bridges, power grids, and communication networks. Floods, even at a local level, can inundate agricultural lands, rendering crops unharvestable and livestock lost, resulting in significant financial strain for farmers and impacting food supply chains. Wildfires, increasingly prevalent in many regions, decimate forests, destroy homes and businesses, and necessitate extensive firefighting efforts, all contributing to massive direct losses. The World Meteorological Organization (WMO) consistently reports on the growing financial toll. In its 2021 report, the WMO highlighted that climate-related disasters in the last decade alone caused approximately $1.5 trillion in economic losses, a stark increase compared to previous decades. This figure is not static; each subsequent year, new records are often set as extreme weather events become more severe and widespread. The interconnectedness of global supply chains means that a disaster in one region can have ripple effects, impacting manufacturing, trade, and consumer prices far beyond the affected area. For example, a significant flood disrupting a major port can lead to delays and increased costs for goods imported and exported globally, affecting businesses and consumers worldwide.

Indirect economic losses, while often harder to quantify precisely, are equally, if not more, significant. These arise from the disruption of economic activity and the loss of earnings. Businesses forced to close due to damage or power outages lose revenue, and their employees lose wages. Supply chain disruptions can lead to shortages and increased prices for goods and services, affecting consumer spending and overall economic output. For instance, a hurricane shutting down a major industrial hub can result in lost production, impacting national GDP. The temporary or permanent closure of businesses, particularly small and medium-sized enterprises (SMEs), can lead to job losses and increased unemployment, requiring government intervention for social support and retraining programs. The tourism industry is particularly vulnerable, with natural disasters deterring visitors and leading to substantial revenue declines for hotels, restaurants, and related businesses. The psychological impact on communities can also contribute to indirect losses, as reduced confidence and increased uncertainty can dampen investment and consumption. Furthermore, the diversion of resources from productive investments to disaster recovery efforts represents a significant opportunity cost, hindering long-term economic growth. The cost of business interruption insurance claims alone can run into billions of dollars annually, underscoring the pervasive nature of these indirect financial burdens. The longer the disruption, the greater the accumulated indirect losses become.

The costs associated with disaster response and recovery are enormous and often strain government budgets. Immediate response efforts involve search and rescue operations, emergency medical services, provision of temporary shelter, food, water, and essential supplies. These require significant personnel, equipment, and logistical coordination. Following the immediate crisis, the recovery phase involves rebuilding damaged infrastructure, providing financial assistance to affected individuals and businesses, and restoring essential services. This can involve substantial public spending on reconstruction projects, often requiring funds that were allocated for other development initiatives. The reliance on international aid can also be a factor for developing nations, but even then, the scale of the need can exceed available resources. The aftermath of a major earthquake or hurricane can necessitate years of rebuilding, with governments often facing difficult decisions about resource allocation and prioritization. The financial burden on public finances can lead to increased national debt, higher taxes, or cuts in other public services. The long-term commitment to disaster recovery can also create a cycle of dependency, where a region becomes perpetually reliant on external assistance for rebuilding rather than developing resilient infrastructure.

Climate change is undeniably a significant driver of escalating natural disaster costs. As global temperatures rise, we are witnessing a marked increase in the frequency and intensity of extreme weather events. Heatwaves are becoming more prolonged and severe, contributing to increased wildfires and heat-related illnesses. Changes in atmospheric circulation patterns are leading to more powerful hurricanes and typhoons, with increased rainfall and storm surge. Shifting precipitation patterns are exacerbating both droughts in some regions and intense flooding in others. The thawing of permafrost in polar regions contributes to sea-level rise, increasing coastal vulnerability to storm surges and erosion. The scientific consensus is clear: human-induced climate change is not a future threat; it is a present reality with tangible and escalating economic consequences. The Intergovernmental Panel on Climate Change (IPCC) reports consistently highlight the link between greenhouse gas emissions and the amplification of extreme weather events. The economic costs of climate change are therefore intricately linked to the costs of mitigating emissions and adapting to a changing climate. The economic models forecasting future losses due to climate change are increasingly dire, suggesting that inaction will lead to exponentially higher costs than proactive measures.

Adaptation and mitigation efforts, while presenting upfront costs, are essential for reducing future disaster-related financial burdens. Adaptation strategies involve adjusting to actual or expected climate change and its effects. This can include building sea walls to protect coastal communities from rising sea levels, developing drought-resistant crops to safeguard agriculture, improving water management systems, and strengthening building codes to withstand extreme weather. Mitigation strategies aim to reduce greenhouse gas emissions to limit the extent of climate change. This involves transitioning to renewable energy sources, improving energy efficiency, and promoting sustainable land use practices. While these measures require substantial investment, they are projected to yield significant economic benefits in the long run by averting or reducing the severity of future disasters. The cost of inaction on climate change, in terms of increased disaster losses, far outweighs the cost of proactive adaptation and mitigation. For example, investing in resilient infrastructure upfront can prevent billions of dollars in damage and recovery costs down the line. The economic argument for climate action is no longer just about environmental protection; it is about financial prudence and long-term economic stability.

The financial sector plays a critical role in managing and absorbing the economic shocks of natural disasters. Insurance companies bear a significant portion of direct economic losses through payouts for property damage, business interruption, and other covered risks. However, as disaster losses escalate, insurers face increasing pressure on their profitability and solvency. This can lead to higher premiums, reduced coverage availability, or even the withdrawal of insurers from high-risk areas. Reinsurance markets, which provide insurance for insurance companies, are also impacted, leading to a global redistribution of risk. The financial stability of the insurance industry is therefore intrinsically linked to the management of natural disaster risk. Furthermore, the availability and affordability of insurance can significantly influence the pace and effectiveness of recovery. In regions with low insurance penetration, individuals and businesses are often left to bear the full brunt of disaster losses, prolonging their financial hardship and hindering economic recovery. The financial sector is also increasingly involved in developing innovative financial instruments, such as catastrophe bonds, to help transfer disaster risk to capital markets.

The economic impact of natural disasters is not evenly distributed. Vulnerable populations and developing countries often bear a disproportionate burden. These communities typically have fewer resources to prepare for, respond to, and recover from disasters. Their housing is often less resilient, their infrastructure is more prone to failure, and their economies are more reliant on climate-sensitive sectors like agriculture. The lack of adequate insurance coverage and social safety nets exacerbates their vulnerability. For instance, a small island developing state, heavily reliant on tourism and agriculture, can be devastated by a single powerful hurricane, setting back its development by years, if not decades. The economic cycle of poverty and vulnerability can be intensified by repeated disaster impacts. The global financial system needs to address these inequities by supporting vulnerable nations with disaster preparedness funding, resilient infrastructure development, and access to financial tools for risk management. International cooperation and targeted aid are essential to build resilience in the most exposed regions.

The increasing economic toll of natural disasters necessitates a paradigm shift in how we approach risk management and economic planning. This includes investing in early warning systems, promoting resilient infrastructure development, implementing robust land-use planning, and fostering community preparedness. The integration of climate change projections into long-term economic development strategies is no longer optional but imperative. Governments, businesses, and individuals must collectively acknowledge the escalating financial risks associated with natural disasters and implement proactive measures to build resilience. The economic future of many regions hinges on their ability to adapt to a changing climate and reduce their vulnerability to extreme weather events. Failure to do so will result in mounting financial burdens that could undermine economic stability and sustainable development on a global scale. The "off the charts" costs are not an abstract future projection; they are a present reality demanding immediate and concerted action.

{kind=link}